May 27, 2022

Osaki Electric Co., Ltd.

The OSAKI Group recognizes that responding to climate change is one of its most important management issues that not only threatens corporate sustainability, but also expands profit opportunities. Accordingly, in November 2021, we announced our support for the Task Force on Climaterelated Financial Disclosures (TCFD) created by the Financial Stability Board (FSB) *1 and joined TCFD Consortium*2. Furthermore, we will disclose information on "Governance," "Strategy," "Risk Management System," and "Indicators and Targets" in line with the recommendations announced by TCFD based on a medium-to long-term perspective that envisages 2030.

*1 TCFD refers to the Climate-Related Financial Disclosure Task Force (Task Force on Climate-related Financial Disclosures) established by the Financial Stability Board (FSB) at the request of the G20. It is recommended that companies and organizations disclose information related to climate change-related risks and opportunities.

TCFD website: https://www.fsb-tcfd.org/

*2 TCFD Consortium is established as a forum for companies and institutions that endorse TCFD recommendations to discuss effective information disclosure and efforts to link disclosed information to appropriate investment decisions by financial institutions, etc.

TCFD Consortium Website: https://tcfd-consortium.jp/

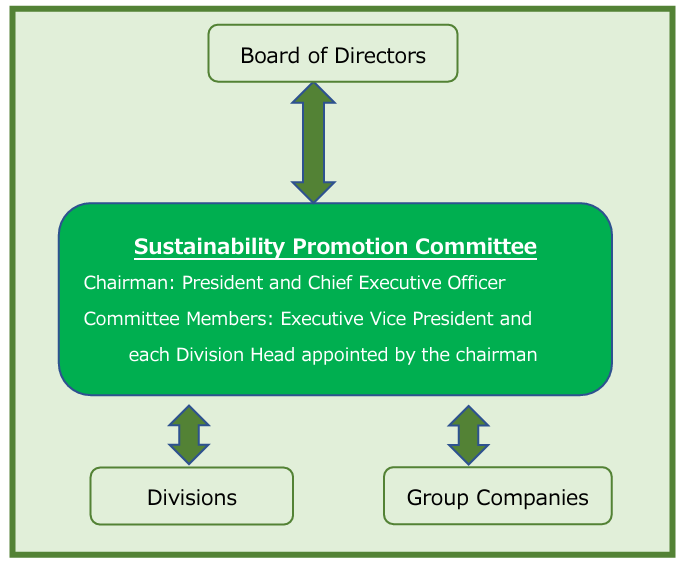

The Sustainability Promotion Committee, chaired by the President and Chief Executive Officer, deliberates on basic policies, important issues, risks, and opportunities related to sustainability, including climate change, and measures to address them. The content of the deliberations is reported to the Board of Directors, and the Board of Directors oversees and supervises sustainability management.

[Organizational Structure for Climate Change Promotion]

Our sustainability promotion system, including climate change, is as follows.

Sustainability Promotion System

OSAKI conducted scenario analysis on how climate change would affect our business using scenarios published by the International Energy Agency (IEA). Specifically, we have summarized anticipated climate change-related risks and opportunities at 2030, applying the 2℃ and 4℃ scenarios. In this analysis, the 2℃ scenario suggests transition risks to maximize, while the 4℃ scenario suggests physical risks to have larger impact.

Transition Risks: Risks arising from the transition to a low-carbon economy, such as the introduction of a carbon tax and the expansion of the emissions trading market Physical risks: Risks posed by intensified natural disasters such as flooding and drought

[Society transitioning to low carbon/decarbonization (2℃ scenario)]

It is a scenario in which strict environmental regulations were introduced to achieve carbon neutrality, resulting in an increase in costs and an anticipated expansion of business opportunities. Physical risks are relatively low and transition risks are high.

[Climate change measures are not implemented and physical risks are actualized (4 ℃ scenario)]

It is a scenario in which no strict environmental regulations or measures are taken. It assumes multiple natural disasters to occur due to an increase in greenhouse gas emissions. Transition risks are low and physical risks are high.

The table below summarizes the significant risks and opportunities that we anticipate will be significantly impacted by climate change, as well as our responses to those risks, in an effort to reduce risks and create opportunities.

Risks

|

Opportunities

|

Based on these analyses, we will reduce the financial impact of climate change on our Group's long-term growth by taking specific measures in each of the risks and opportunities. We are currently assessing the possible impact on earnings in 2030 based on information obtained through scenario analysis.

In order to ensure the sustainable and stable development of our business, our group identifies, analyses and evaluates risks, and takes necessary measures to reduce identified risks. We regard climate change as an important risk and are promoting specific measures based on the Osaki Electric Group Basic Sustainability Policy.

OSAKI aims to reduce greenhouse gas emissions related to Scope 1 and 2 by 46% in fiscal 2030 compared to fiscal 2013. At the same time, we aim to achieve carbon neutrality by 2050 based on “ Green Growth Strategy Through Achieving Carbon Neutrality in 2050” formulated by the Japanese Government, among other measures. With regard to Scope3, we are working to refine our aggregation in order to set targets, and aim to acquire SBTs (Science Based Targets).

Notes

Scope1: CO2 emissions from fuel-use by businesses themselves

Scope2: CO2 emissions from the use of electricity supplied by other companies

Scope3: Indirect emissions other than Scope1 and Scope2 (emissions by other companies related to the business activities of the company)